Following the recent announcement that the secondary market for life insurance grew by 19% in 2017, we've taken calls from a number of advisors wanting to discuss potential cases.

Some calls came from financial professionals who previously had been sitting on the sidelines while weighing the market's stability and regulatory environment.

It seems that many professional advisors are viewing life settlements in a whole new light. As part of their due diligence efforts, some estate planning professionals and CPAs tell us they now consider it their fiduciary duty to inform clients of the life settlement option when the situation warrants it.

Convinced — but Confused

Many professional advisors recognize that their valued clients are entrusting them to maximize the market price of their insurance asset and to execute the transaction in a fully transparent and compliant manner. Clients want to know that they can sell with confidence — while leaving no money on the table.

Although more professional advisors are convinced that in certain situations a life settlement is the most favorable (and lucrative) exit strategy for an unwanted policy, some advisors are not clear on which path to take as it relates to selling their clients' policies. Should they sell a policy directly to a provider (buyer) as they've seen on TV? Or, should they partner with a life settlement broker who will initiate an auction process to elicit competing bids from multiple providers in pursuit of the highest offer?

We consider it a privilege to be on the calling list of professional advisors whose due diligence efforts involve interviewing life settlement brokers. We also respect the fact that, as highly accomplished attorneys, CPAs, and estate planning professionals, they demand straight talk and well-reasoned responses.

As experienced life settlement brokers, we obviously believe it is in the seller's best interests to shop the policy to multiple buyers before accepting an offer. Without going through the auction process of allowing multiple providers to submit competing bids in an effort to determine the highest possible offer, the seller may be left wondering whether their policy could have been worth more.

The Role of the Broker

When it comes to educating professional advisors and consumers about whether to sell a policy directly to a provider or use a broker, the best approach may be to present both sides of the argument as objectively as possible and let the student decide. As discussed below, we're confident that the value that the broker brings will speak for itself.

Life settlement brokers have a fiduciary duty to represent the policy seller's interests.

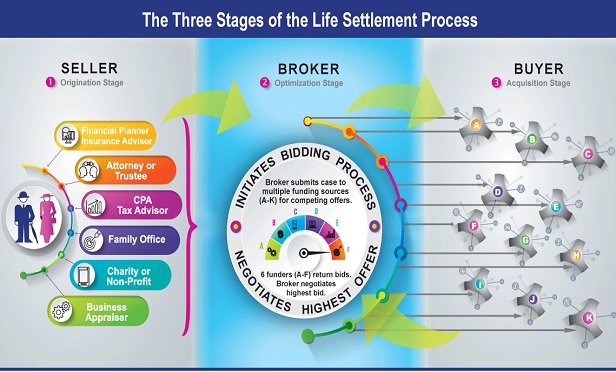

As illustrated in our infographic, the 3 Stages of the Life Settlement Process (shown above, and also on our own site), the broker is an integral partner in each life settlement transaction.

Our diagram shows that the primary function of the settlement broker is to submit the seller's policy to multiple money sources (providers) in order to create a bidding competition in pursuit.

Jeff Hallman is aco-founder and managing partner at Asset Life Settlement LLC. He began his career in life settlements in 2001 and since then has negotiated transactions valued at about $2 billion in face value. He has been involved in case submission, underwriting, compliance, the institutional bidding process, life expectancy analyses and contract negotiation in the life settlement market. He can be reached at [email protected] or 888-335-4769 x1108.

Scott Thomas is a co-founder and managing partner at Asset Life Settlements LLC. He began his career in the life settlement industry more than 15 years ago and has since transacted about $2 billion in policy face value. He has worked on transactions involving multimillion-dollar policies involving complex estate plans. He can be reached at [email protected] or 888-335-4769 x1115.

(Image: Asset Life Settlements LLC)

(Image: Asset Life Settlements LLC)  Jeff Hallman is a co-founder and managing partner at

Jeff Hallman is a co-founder and managing partner at